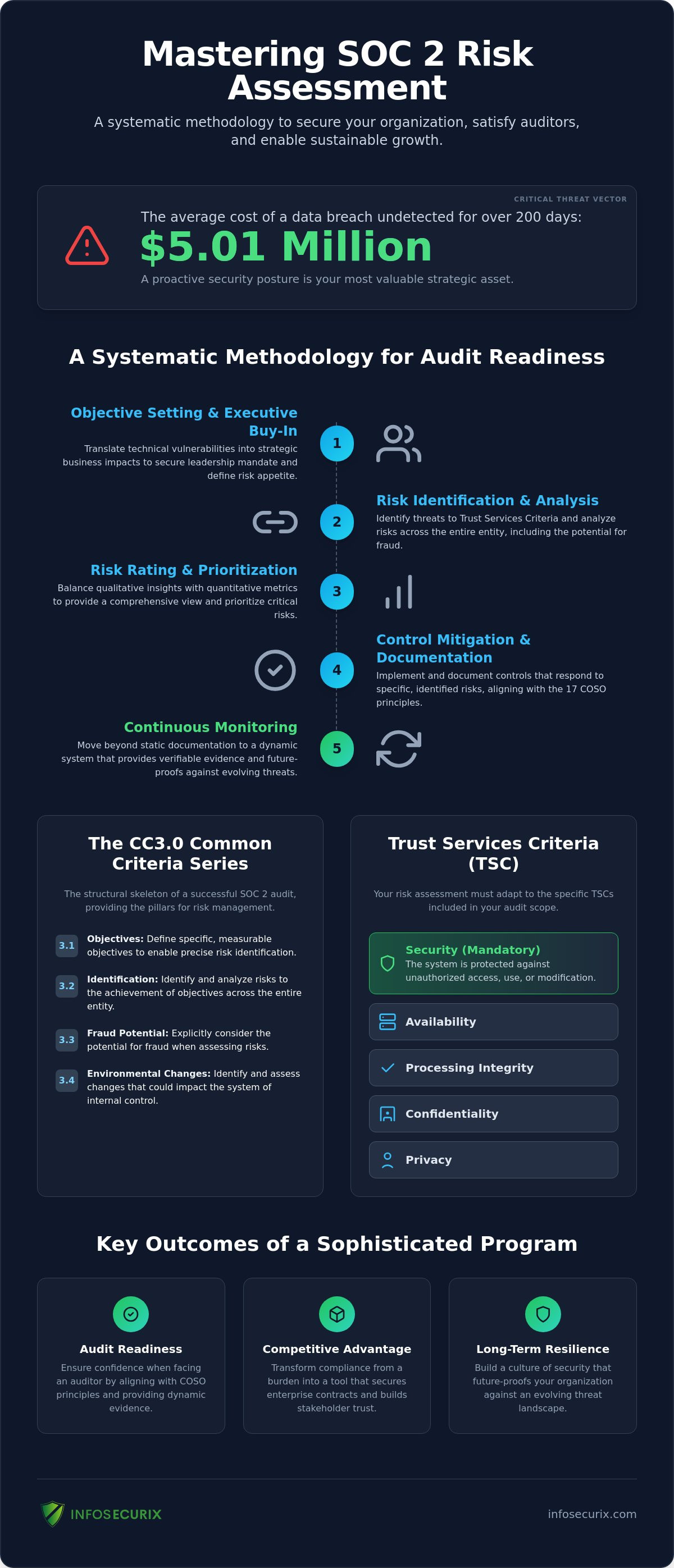

A data breach that remains undetected for more than 200 days now carries a staggering average cost of $5.01 million, making a proactive security posture your most valuable strategic asset. You likely recognize the growing complexity of the AICPA Trust Services Criteria and feel the challenge of translating technical vulnerabilities into clear business impacts. Developing a sophisticated SOC 2 risk assessment methodology serves as more than a compliance checklist; it’s an empowering framework that secures your organization’s reputation and enables sustainable growth.

We understand the need for absolute confidence when facing an auditor, especially as expectations shift toward dynamic evidence and rigorous AI governance. This guide provides the clarity you need to master the identification and mitigation of institutional risks while ensuring your documentation remains audit-ready. You’ll learn to align your controls with CC3.0 requirements and integrate the 2026 COSO guidance on Generative AI. We’ll preview a repeatable process that moves your compliance program from a static manual to a sophisticated system of continuous monitoring.

Key Takeaways

- Master the systematic process of identifying threats to the Trust Services Criteria: a mandatory requirement under the CC3.0 series that forms the bedrock of your compliance posture.

- Implement a structured SOC 2 risk assessment methodology that balances qualitative insights with data-driven quantitative metrics to provide a comprehensive view of institutional risk.

- Secure essential executive buy-in by translating granular technical vulnerabilities into strategic business impacts during the initial objective-setting phase.

- Ensure audit readiness by explicitly aligning your internal control framework with the 17 COSO principles adopted by the AICPA.

- Move beyond static documentation toward a state of continuous monitoring: it’s the key to future-proofing your organization against the evolving threat landscape of 2026.

The Foundational Role of Risk Assessment in SOC 2 Compliance

A sophisticated SOC 2 risk assessment methodology serves as the intellectual engine of your entire compliance program. This methodology represents the systematic process of identifying, evaluating, and managing threats to the AICPA Trust Services Criteria (TSC). Rather than viewing this as a mere administrative hurdle, we see it as a vital diagnostic tool that provides a clear-eyed view of how vulnerabilities could impact your organization’s most sensitive data assets. By grounding your security posture in the broader System and Organization Controls (SOC) framework, you establish a baseline of operational integrity that resonates with sophisticated enterprise partners and stakeholders alike.

The AICPA mandates this rigorous scrutiny under the Common Criteria, specifically within the CC3.0 series. This requirement ensures that organizations don’t just implement controls in a vacuum; they must demonstrate that every safeguard responds to a specific, documented risk. Adopting a “Risk-First” culture, a philosophy we advocate for at InfoSecurix, transforms compliance from a seasonal burden into a formidable competitive advantage. In the high-stakes environment of 2026 enterprise sales, the ability to prove a proactive stance against evolving threats often becomes the deciding factor in securing lucrative contracts. It’s about moving beyond the “check-the-box” mentality to build a culture of long-term resilience.

Understanding the CC3.0 Common Criteria Series

The CC3.0 series functions as the structural skeleton of a successful SOC 2 audit report, providing the necessary pillars for risk management. It is divided into four critical components that every organization must address:

- CC3.1: Defining specific, measurable objectives to enable the precise identification and assessment of risks.

- CC3.2: Identifying and analyzing risks to the achievement of those objectives across the entire entity.

- CC3.3: Explicitly considering the potential for fraud, including internal and external pressures, when assessing risks.

- CC3.4: Identifying and assessing changes in the business environment that could significantly impact the system of internal control.

These criteria dictate how an organization must perceive and respond to its unique threat landscape to maintain a stable and trustworthy control environment.

The Interplay Between Risk and the Trust Services Criteria

Your chosen SOC 2 risk assessment methodology must remain fluid, adapting to the specific Trust Services Criteria you choose to include in your audit scope. While Security remains the mandatory core, adding Availability, Processing Integrity, Confidentiality, or Privacy requires a more nuanced approach to risk identification. A unified methodology allows you to address these overlapping requirements simultaneously, creating a cohesive narrative of resilience that satisfies both auditors and clients. For a deeper dive into preparing your organization for this level of scrutiny, consult our Strategic SOC 2 Readiness Checklist. This roadmap ensures that your risk assessment isn’t just a point-in-time exercise but a cornerstone of enduring enterprise trust.

A Systematic Methodology: From Asset Identification to Mitigation

Establishing a strategic SOC 2 risk assessment methodology requires more than a casual glance at your IT environment. It demands a disciplined, multi-phase workflow that ensures no vulnerability remains hidden from view. This process starts with executive buy-in during the objective-setting phase. When leadership defines the organization’s risk appetite, they provide the necessary mandate for the entire security team to act with precision. We treat the resulting risk register as a living document; it’s a dynamic record that maintains audit evidence throughout the year rather than a static file gathering digital dust. Auditors in 2026 are increasingly rejecting static screenshots in favor of verifiable, dynamic evidence, making this continuous approach essential for a successful attestation.

A professional standard in this field involves distinguishing between inherent risk and residual risk. Inherent risk represents the raw threat level before any safeguards are active. Residual risk is what remains once your controls are functioning. Demonstrating this gap to an auditor proves that your security investments are delivering measurable value and that your control environment is robust enough to handle modern threats.

Phase 1: Asset Inventory and Criticality Mapping

Identify every information asset within your ecosystem: data repositories, hardware, and subservice organizations. Assign a criticality score to each based on the potential business impact of a breach. This mapping is essential for defining your audit scope, a topic we explore further in our guide on information security risk assessment. Understanding which assets are vital to your Trust Services Criteria allows you to prioritize resources where they matter most.

Phase 2: Threat Modeling and Vulnerability Analysis

Identify internal and external threats. These range from sophisticated cyber-attacks to simple human error or environmental disasters. Analyze which vulnerabilities within your existing controls these threats might exploit. To maintain a high level of precision, we recommend using a framework for calculating likelihood and impact scores, similar to the NIST Risk Management Framework. This rigorous approach to your SOC 2 risk assessment methodology ensures that your defense strategy remains grounded in globally recognized best practices.

Phase 3: Strategic Risk Response Selection

Once risks are scored, you must choose a response based on four professional pillars:

- Mitigation: Deploying controls to reduce the risk to an acceptable level.

- Acceptance: Formally acknowledging a low-impact risk when the cost of mitigation outweighs the potential loss.

- Transference: Shifting the risk to a third party, such as through cyber insurance providers.

- Avoidance: Eliminating the risk by ceasing the associated business activity entirely.

Documenting the rationale for each choice is critical. An auditor doesn’t just want to see that you’ve identified a risk; they want to see the logic behind your response. If you’re unsure how your current controls stack up against these pillars, a professional SOC2 Readiness Assessment can provide the necessary clarity to move forward with confidence.

Qualitative vs. Quantitative: Selecting the Right Risk Rating Framework

Selecting the appropriate rating framework is a pivotal decision in your SOC 2 risk assessment methodology. This choice dictates how you communicate threats to stakeholders and how you justify security expenditures to the board. While some organizations prefer the intuitive nature of qualitative labels, others require the mathematical precision of quantitative data. We often guide our clients toward a methodology that matches their specific maturity level; it’s about ensuring the framework is sophisticated enough to be useful but simple enough to be executed consistently. A fragmented approach where different departments use conflicting scales is a significant red flag for auditors. Consistency remains the hallmark of a professional control environment.

Many high-growth organizations find a semi-quantitative hybrid model to be the most effective path for SOC 2 compliance. This approach assigns numerical values to qualitative tiers, allowing for a degree of data aggregation without requiring the exhaustive resource investment of a full actuarial analysis. By bridging the gap between “High/Medium/Low” and specific risk scores, you provide the auditor with a logical, repeatable process that demonstrates a deep understanding of your institutional threat landscape.

The Case for Qualitative Assessment in Early Compliance

Qualitative models offer unparalleled speed and accessibility for organizations pursuing their first SOC 2 attestation. These frameworks rely on the expertise of Subject Matter Experts (SMEs) to validate risk ratings based on their professional experience. To avoid the subjectivity trap, we recommend using clearly defined rubrics that specify exactly what constitutes a “High” impact. For example, a “High” impact might be defined as any event that results in a service outage exceeding four hours or compromises the personal data of more than 1,000 users. This level of precision transforms a subjective opinion into a defensible audit artifact.

Advancing to Quantitative Models for Enterprise Maturity

Enterprise-level organizations often transition to quantitative models to align security spending with broader business objectives. By assigning dollar values to potential risks, leadership can make informed decisions based on the expected financial impact of a breach. The FAIR (Factor Analysis of Information Risk) framework stands as a professional standard in this space; it provides a rigorous structure for analyzing risk in financial terms. It’s important to remember that for a SOC 2 audit, the auditor is less concerned with the exact dollar amount and more focused on the integrity of the methodology used to reach it. They want to see that your numbers are rooted in a logical, documented process rather than arbitrary estimates.

Satisfying the Auditor: Aligning with COSO Principles and Common Criteria

A frequent question we encounter from executive leadership is why a standard IT risk assessment doesn’t suffice for a SOC 2 audit. The distinction is critical: while technical vulnerability scans identify software flaws, a comprehensive SOC 2 risk assessment methodology must address the broader organizational governance required by the AICPA. This methodology must explicitly link to the 17 COSO Principles that form the bedrock of the Trust Services Criteria. These principles ensure that your internal controls are not just a collection of technical tools but a cohesive system of governance that supports your business objectives. Auditors look for this alignment to verify that your security posture is integrated into the very fabric of your organization.

During an audit walk-through, your assessor will demand verifiable evidence of this integrated approach. They expect to see a documented journey from risk identification to mitigation: a trail that includes risk registers, meeting minutes, and evidence of corrective actions. The most vital piece of evidence is often the Management Review. This high-level scrutiny proves that senior leadership is actively involved in the risk management process, demonstrating the “tone at the top” that auditors find so reassuring. Without this executive oversight, your assessment remains a technical exercise rather than a strategic audit artifact.

Addressing Fraud Risk and Misconduct (CC3.3)

Auditors specifically look for how your organization identifies and responds to the potential for fraud. This involves analyzing “incentives, pressures, and opportunities” that could lead to misconduct. We advocate for integrating fraud risk directly into your broader security assessment to avoid the inefficiency of separate silos. You should document specific controls designed to mitigate these risks, such as:

- Segregation of Duties: Ensuring no single individual has end-to-end control over a sensitive business process.

- Whistleblower Policies: Providing a secure, anonymous channel for reporting unethical behavior.

- Rigorous Background Checks: Verifying the integrity of individuals before granting access to critical systems; for those with Brazilian operations, you can learn more about Verifica Processo to see how legal consultation platforms assist in verifying the legal history of individuals and entities.

Managing Internal and External Changes (CC3.4)

Your methodology must also account for the risks that arise from organizational evolution. Whether you are adopting a new cloud provider or navigating a complex acquisition, every shift in your tech stack or business structure introduces new vulnerabilities. A robust internal audit process serves as your first line of defense, identifying gaps in change management before they become audit failures. It is a professional necessity to re-evaluate your risk profile whenever a significant operational shift occurs to ensure your controls remain effective.

Prepare your organization for the scrutiny of a modern audit. Connect with our experts to conduct a comprehensive Risk Assessment that aligns your controls with global standards.

Beyond the Methodology: Partnering for SOC 2 Readiness and Resilience

Mastering the technical nuances of a SOC 2 risk assessment methodology is a significant achievement, yet the true value of this exercise lies in how it informs your broader business strategy. Transitioning from a theoretical framework to a functional, resilient security posture requires more than just templates or automated tools. It demands a partnership with a seasoned guide who can translate complex requirements into actionable business intelligence. We encourage you to view compliance not as a final destination or a yearly hurdle, but as a continuous state of operational excellence that safeguards your organization’s reputation and enables sustainable growth.

With over 25 years of experience in professional services, InfoSecurix serves as a protective force and the ultimate safeguard against the surprises that often derail audit timelines. Our deep-rooted knowledge allows us to anticipate auditor inquiries and address them before they become formal findings. A professional SOC 2 readiness assessment leverages your existing risk methodology to build a precise roadmap for remediation. This process ensures that every control you implement is both effective and defensible during the final walk-through, providing you with absolute confidence in your audit readiness.

The InfoSecurix Approach to Tailored Risk Frameworks

We pride ourselves on delivering a bespoke experience that stands in stark contrast to the generic, automated “compliance-in-a-box” solutions currently flooding the market. While software can collect data, it cannot provide the strategic corrective actions necessary for complex SaaS or enterprise environments. Our Trusted Advisor relationship ensures that your SOC 2 risk assessment methodology evolves alongside your business. We don’t just identify gaps; we work collaboratively to implement sophisticated solutions that maintain the integrity of your SOC 2 report for years to come. This high-level register of service ensures that your technical processes always align with your strategic impact.

Securing Your Enterprise Legacy

Securing your enterprise legacy requires a commitment to meticulous standards and a visionary approach to cybersecurity. The peace of mind that comes from a methodology validated by seasoned experts allows your leadership team to focus on innovation while we manage the complexities of the Trust Services Criteria. Our focus remains on future-proofing your posture against the emerging threats of 2026 and beyond. By establishing a steady and reliable control environment today, you enable the long-term success and scalability of your organization.

Engage InfoSecurix for your SOC 2 Readiness Assessment today.

Future-Proofing Your Compliance Strategy

Building a resilient organization starts with a robust SOC 2 risk assessment methodology that evolves alongside your business. You’ve learned that aligning with the CC3.0 series and the 17 COSO principles is more than an audit requirement; it’s a strategic framework for protecting your enterprise legacy. By shifting from static documentation to a culture of continuous monitoring, you ensure that your security posture remains effective against the sophisticated threats of 2026.

InfoSecurix brings over 25 years of information security expertise to your side, acting as a seasoned guide through the complexities of the audit process. Our bespoke methodology is tailored to your unique business scope, ensuring that your controls are both rigorous and practical. We take pride in our 100% audit success rate for readiness clients, providing the absolute confidence you need to secure your market position. Secure your enterprise trust with a professional SOC 2 Readiness Assessment from InfoSecurix.

Your commitment to these meticulous standards today will pave the way for a secure and prosperous future.

Frequently Asked Questions

What is the difference between a SOC 2 risk assessment and a standard IT risk assessment?

A SOC 2 risk assessment methodology differs from a standard IT assessment by focusing explicitly on the AICPA Trust Services Criteria and the 17 COSO principles. While a technical assessment might identify server vulnerabilities, a SOC 2 assessment evaluates how those risks impact the broader control environment and business objectives. It requires a holistic view of governance, fraud potential, and organizational change rather than just technical flaws.

How often should a SOC 2 risk assessment be performed?

You should perform a risk assessment at least annually to remain compliant with SOC 2 standards. However, professional best practices dictate that you must re-evaluate your risk profile whenever a significant operational change occurs; this includes cloud migrations, acquisitions, or the introduction of new technology like generative AI. This continuous approach ensures your controls remain effective throughout the entire audit period.

Does the AICPA require a specific risk assessment framework like NIST or ISO?

The AICPA does not mandate a specific framework like NIST or ISO, although it requires that your methodology align with COSO principles. You have the flexibility to choose a framework that suits your organization’s maturity, provided it’s applied consistently across all departments. Auditors look for a logical, repeatable process that demonstrates a deep understanding of your threat landscape rather than the use of one specific global standard.

Can we use automated software to conduct our SOC 2 risk assessment?

You can use automated compliance platforms to streamline data collection, but software alone cannot satisfy an auditor’s requirement for professional judgment. Automated tools often lack the context needed to assess complex business impacts or specific fraud risks. A successful SOC 2 risk assessment methodology requires expert oversight to validate the data and ensure the resulting risk register reflects your actual operational reality.

What are the most common “red flags” auditors find in risk assessment methodologies?

Auditors frequently identify red flags such as static risk registers that haven’t been updated in over a year or a total lack of executive review. Another common failure is ignoring the CC3.3 and CC3.4 criteria; specifically fraud risk and organizational change management. If your documentation doesn’t show a clear link between a specific risk and its corresponding control, the auditor will likely question the integrity of your entire program.

How do we document risk acceptance to satisfy a SOC 2 auditor?

Documenting risk acceptance requires a formal record that includes the rationale for the decision and an official sign-off from senior leadership. You must explain why the cost of mitigation outweighs the potential impact and confirm that the residual risk falls within the organization’s defined appetite. This transparency demonstrates to the auditor that the decision was a deliberate strategic choice rather than an oversight or a failure to act.

What role does the Board of Directors play in the risk assessment process?

The Board of Directors provides essential oversight by reviewing the results of the risk assessment and ensuring that the organization’s risk appetite aligns with its long-term goals. They are responsible for establishing the “tone at the top,” which signals to the entire organization that security and compliance are high priorities. Their active involvement serves as powerful evidence of a mature governance structure during an audit walkthrough.

Is a vendor risk assessment a mandatory part of SOC 2 compliance?

Vendor risk assessment is a mandatory component of SOC 2 compliance, particularly under the Security and Confidentiality criteria. You must demonstrate a systematic process for evaluating the security posture of subservice organizations that handle your sensitive data. Auditors in 2026 are placing increased scrutiny on supply chain risks, making it vital to include third-party vulnerabilities in your broader methodology to ensure comprehensive resilience.